There are few moments more stressful than checking your phone and spotting a notification for a huge transaction you never made, especially from another country. For a long time, digital payments felt risky, almost like trusting an unseen system with your hard-earned money. If your card has ever been blocked just because you used it in another city, you already know how inconvenient and slow traditional security methods used to be.

Now in 2026, things feel very different. The old system of manual checks and fixed rules has quietly faded away. Today, every tap, swipe, or online payment is protected by an intelligent system working silently in the background. Artificial intelligence now acts like a personal security guard for your money, constantly learning your habits and protecting you without interrupting your experience.

Basic Concepts: Understanding AI in Payment Security

To see how big this shift is, it helps to understand how fraud detection worked earlier. Banks relied on strict rule-based systems. For example, a rule might say, “Block any transaction above $1,000 at 3:00 AM.” While this could stop some fraud, it also blocked genuine purchases. Someone ordering food late at night or buying something during travel could get stuck unnecessarily. At the same time, smart fraudsters easily found ways to avoid these basic rules.

Artificial intelligence, especially Machine Learning (ML), works differently. Instead of following fixed instructions, it learns from data. It studies millions of transactions, both genuine and fraudulent, and gradually understands patterns that humans might miss.

This smart layer of protection is a key part of shaping the future of AI in banking, making digital payments not just secure but also smooth for everyday users.

The Core Explanation: Moving from Rules to Real-Time Context

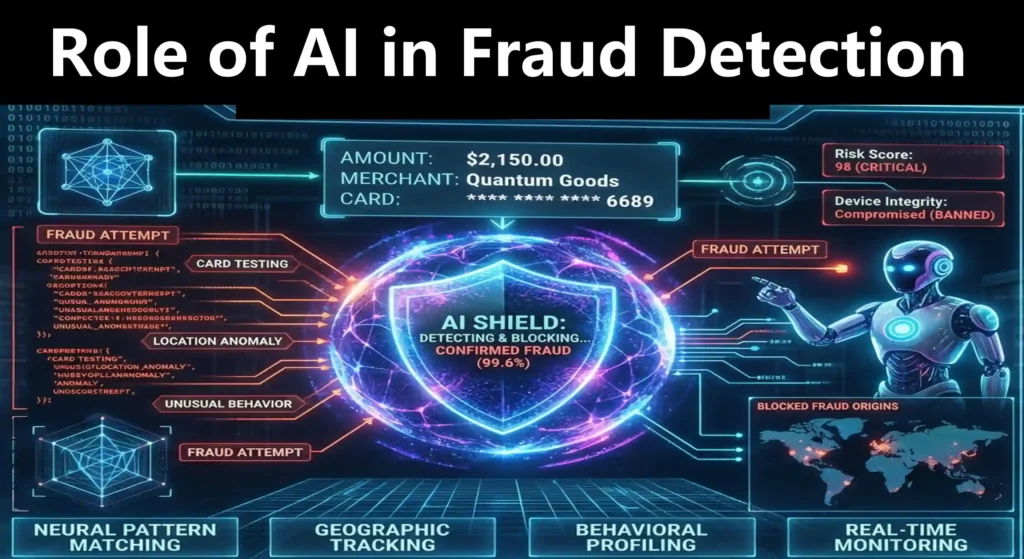

The real strength of AI comes from its ability to understand context. When you make a payment, it does not just check the amount or the store. It evaluates hundreds of signals instantly.

It looks at your device location, how fast you type, how you usually hold your phone, and your past spending behavior. For example, if you usually shop at local stores on weekends in India, and suddenly a luxury purchase appears from another continent late at night, the system quickly flags it.

At the same time, it does not overreact. Suppose you suddenly book flight tickets or buy something expensive during a festival sale. The system understands that such behavior can be normal. This balance between caution and flexibility is what makes AI-driven fintech so effective, protecting money while keeping the experience hassle-free.

How It Works: The Step-by-Step Security Process

Every time you click “Pay,” a detailed process runs in the background within milliseconds. Here is how AI evaluates each transaction:

Step 1: Data Ingestion

As soon as the payment starts, the system collects all relevant data. This includes transaction details, device information, location, and network signals.

Step 2: Feature Extraction

The system converts this raw data into measurable points. For example, it checks how far your current location is from your last transaction and whether it is physically possible to travel that distance in that time.

Step 3: Algorithmic Scoring

These data points are processed by machine learning models. The system compares your transaction with known fraud patterns and your personal history. It then assigns a risk score between 1 and 100.

Step 4: The Autonomous Decision

Based on the score, the system decides instantly. It may approve the transaction, block it, or ask for additional verification such as an OTP or biometric check.

Types and Components of AI Fraud Systems

Banks and payment companies use multiple AI systems together to create strong protection.

- Supervised Machine Learning: These models learn from labeled data and are effective at detecting known fraud patterns.

- Unsupervised Machine Learning: These systems identify unusual behavior in raw data and help catch new types of fraud.

- Natural Language Processing (NLP): This scans messages and emails to detect phishing or scam attempts before transactions happen.

- Behavioral Biometrics: This tracks how you interact with your device. Even if someone knows your password, they cannot copy your exact touch and usage pattern.

Features and Benefits: Why AI Wins

Using AI in payment systems has improved both safety and convenience.

1. Drastic Reduction in False Positives

A false positive happens when your genuine transaction gets blocked. Earlier, this was common and frustrating. Now, AI understands your behavior better, so such interruptions have reduced significantly.

2. Millisecond Response Times

Fraudsters try to act fast. AI responds even faster. It analyzes and takes action within milliseconds, stopping suspicious activity immediately.

3. Adaptive Continuous Learning

Unlike older systems, AI keeps learning. If a new scam appears somewhere in the world, the system updates itself quickly and applies that knowledge globally.

Real-World Use Cases: AI in Action

Let us look at how this works in real situations.

Imagine someone traveling frequently and using an API wallet. Earlier, using public Wi-Fi in airports or making large purchases abroad could freeze the account. Now, the system checks travel data, device identity, and usage patterns before allowing the payment smoothly.

In another case, think of a small Indian business owner running an online store during festive sales like Diwali. If attackers try to test stolen cards on the website, the AI detects unusual activity patterns and blocks those attempts instantly, without affecting genuine customers.

Comparison Table: Traditional vs. AI Fraud Detection

| Feature | Traditional Rules-Based Systems | AI-Powered Detection Systems |

|---|---|---|

| Decision Making | Rigid, static “If/Then” parameters. | Dynamic, context-aware machine learning. |

| Speed of Adaptation | Requires manual coding updates. | Learns and adapts autonomously in real-time. |

| False Positive Rate | Very High (frequent unnecessary card blocks). | Very Low (understands normal behavioral shifts). |

| Data Analysis | Limited to basic transaction details. | Analyzes thousands of hidden data points. |

| New Threat Detection | Fails against unknown, novel attacks. | Identifies anomalies to catch zero-day fraud. |

Security, Risks, and Challenges

Even though AI is powerful, it is not perfect. There are still challenges that need attention.

Adversarial Artificial Intelligence

Fraudsters are also using AI. They test systems repeatedly to find weak points or use fake voices to bypass security. Staying updated with cybersecurity trends for 2026 is important as this competition continues.

Data Privacy Concerns

AI needs large amounts of data to work effectively. This raises concerns about privacy. Many users worry about how their information is used, especially with discussions around the death of personal privacy. Strong encryption and privacy-focused systems are essential.

The “Black Box” Problem

Sometimes even developers cannot fully explain why an AI system made a specific decision. If a genuine transaction is blocked without a clear reason, it can reduce trust and create regulatory issues.

Best Practices for Consumers and Businesses

Even with AI, users also need to follow good practices to stay safe.

- Enable Biometrics Everywhere: Move beyond passwords. Using biometric finance in 2026 adds an extra layer of protection.

- Maintain Consistent Digital Hygiene: Avoid unnecessary use of VPNs while accessing banking apps, as changing locations frequently can trigger alerts.

- Layer Your Security: Use virtual cards for online purchases. This helps protect your main account from risks like the digital currency trap.

Advanced Concepts: Federated Learning and Graph Networks

Some advanced technologies are making these systems even stronger.

Federated Learning allows different banks to improve a shared AI model without sharing actual customer data. Each bank trains the model locally and only shares insights, not sensitive information.

Graph Neural Networks (GNNs) focus on connections between accounts, devices, and transactions. They help detect large fraud networks by identifying patterns across multiple linked activities.

These technologies will play an important role as systems like Central Bank Digital Currencies (CBDCs) become more common.

Future Trends: What Lies Beyond 2026?

Fraud detection is moving towards prediction. Soon, systems may stop fraud before it even happens by analyzing patterns from different sources, including hidden online networks.

In the coming years, protection will become even stronger with the use of quantum cryptography. This will make digital payment systems extremely secure against hacking attempts.

Conclusion

Artificial intelligence has changed how digital payments are secured. What was once a slow and risky process has now become fast and reliable. By understanding behavior and adapting in real time, AI has made financial systems safer for everyday users.

Even though cyber threats will continue to evolve, the systems protecting your money are improving at a faster pace. Today, you can make digital payments with much more confidence, knowing that a smart system is constantly working in the background to keep your finances safe.