In 2026, the performance of a graphics card is no longer dictated solely by the GPU die. Instead, the Memory Subsystem has become the primary differentiator. With the world currently facing what industry insiders call the “RAMpocalypse”—a global shortage driven by AI data center demand—the “Big Three” memory fabbers are fighting for every square millimeter of silicon wafer.

Whether you are a gamer looking at GDDR7 for your next rig or an enterprise architect scouting HBM4, understanding who leads the market is critical for predicting price and availability.

1. The State of the Market: 2026 Market Share

As we enter the first quarter of 2026, the market share has shifted dramatically due to the AI supercycle. While Samsung remains the volume king in general DRAM, SK Hynix has seized the lead in high-value AI memory (HBM).

Market Growth: HBM Market Share (Q1 2026)

SK Hynix continues to dominate the high-bandwidth memory sector as NVIDIA’s primary partner for the Rubin platform.

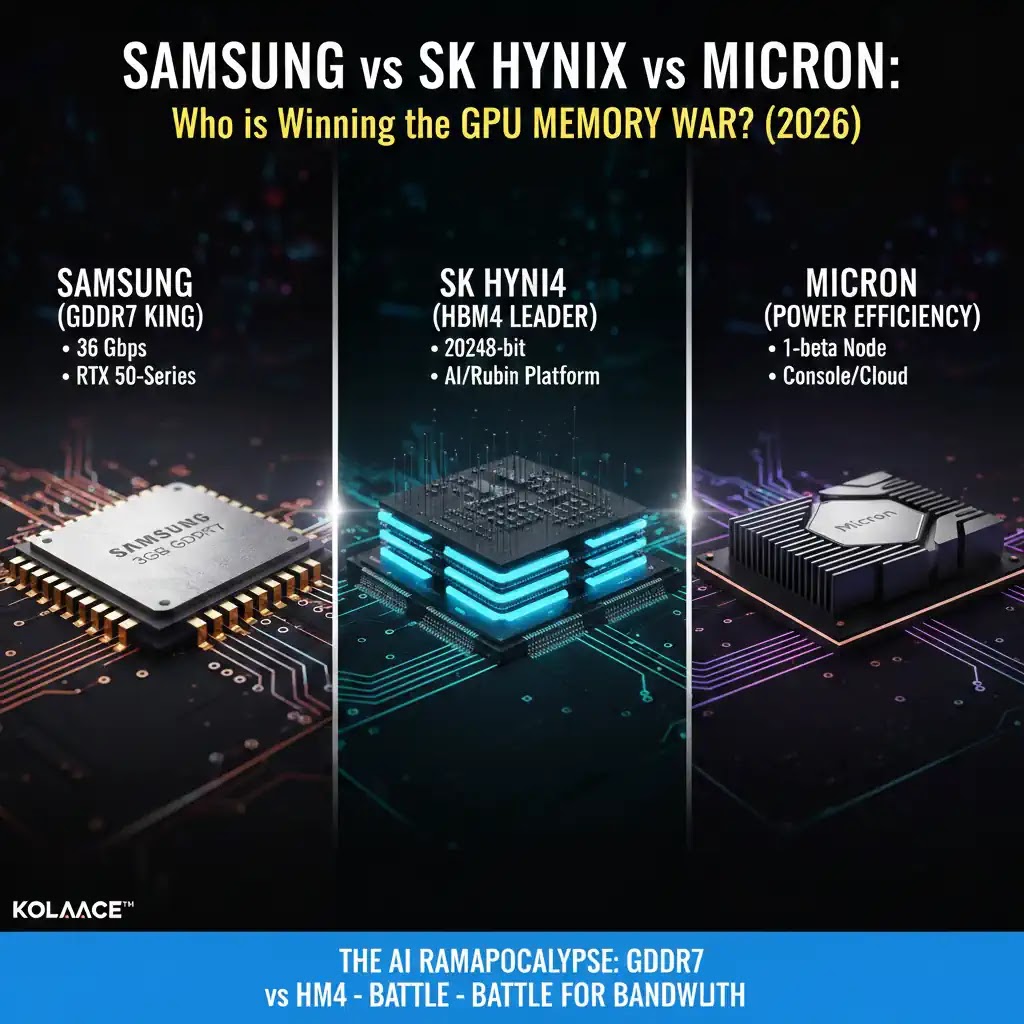

2. Technology Comparison: GDDR7 vs. HBM4

The “war” is fought on two fronts: the consumer market (GDDR7) and the AI/Data Center market (HBM4).

| Feature | Samsung | SK Hynix | Micron |

|---|---|---|---|

| GDDR7 Status | Mass Production (28-36 Gbps) | Sampling (48 Gbps peak) | Mass Production (32 Gbps) |

| HBM4 Roadmap | Feb 2026 Production Start | Sept 2026 Production Start | 2027 Roadmap |

| Key Advantage | Highest Manufacturing Capacity | TSMC Packaging Synergy | Best Power Efficiency (1-beta) |

— KOLAACE™ Market Report

3. The “Rubin” Factor: NVIDIA’s Choice

NVIDIA’s upcoming Vera Rubin architecture is the ultimate prize. Reports indicate that SK Hynix and Samsung have both secured spots for HBM4 supply, while Micron is focusing on hyperscale cloud providers. For gamers, Samsung has emerged as the primary provider for 3GB GDDR7 modules, which are expected to power the “SUPER” refresh of the RTX 50-series later this year.